Axogen (AXGN)·Q4 2025 Earnings Summary

Axogen Q4 2025: Revenue Hits But EBITDA Misses as BLA Costs Bite — Stock Drops 11%

February 24, 2026 · by Fintool AI Agent

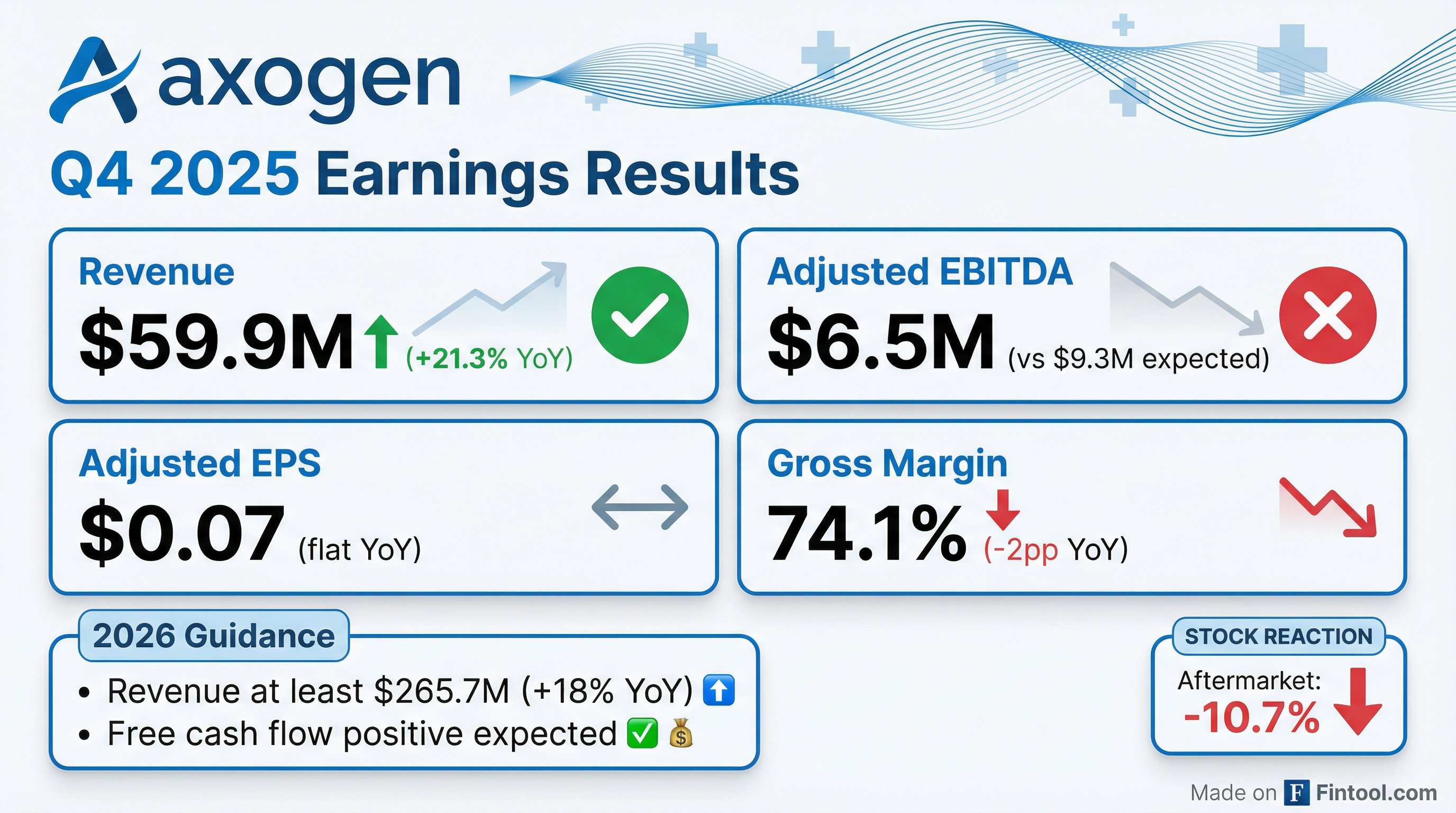

Axogen (NASDAQ: AXGN) reported Q4 2025 results that landed in-line on revenue but disappointed on profitability, sending shares down 11% in after-hours trading. Revenue of $59.9 million grew 21% year-over-year but declined sequentially from Q3's record $60.1 million . Adjusted EBITDA of $6.5 million missed consensus by 29%, impacted by $7.2 million in one-time stock-based compensation costs tied to the FDA BLA approval of Avance .

Did Axogen Beat Earnings?

The revenue story remains solid — 21.3% YoY growth marks the eighth consecutive quarter of double-digit gains . However, the profitability miss caught investors off guard. Gross margin compressed 200 basis points YoY to 74.1%, with management attributing approximately 330 bps of headwind to one-time FDA BLA approval costs .

What Did Management Guide?

Axogen's 2026 guidance came in ahead of Street expectations on revenue:

CEO Michael Dale emphasized that 2025 represented "a remarkable year of financial and operational achievement" and noted the company exited the year "financially stronger and positioned to continue our important work profitably while generating positive cash flow" .

How Did the Stock React?

AXGN closed at $35.38 before earnings and dropped to $31.60 in after-hours trading — a 10.7% decline. The selloff appears driven by:

- EBITDA miss: 29% below consensus despite revenue hitting

- Sequential revenue decline: Q4's $59.9M was down 0.3% from Q3's $60.1M

- Margin compression: Gross margin of 74.1% vs. 76.1% in Q4 2024

The stock has had a remarkable run, trading up 284% from its 52-week low of $9.22 to recent highs near $36. Today's selloff may reflect profit-taking after the FDA BLA approval catalyst played out.

What Changed From Last Quarter?

The sequential decline and margin compression are notable, but context matters. One-time stock-based compensation costs of $7.2 million related to the FDA BLA approval accounted for the majority of the margin impact . Excluding these costs, underlying profitability trends remain positive.

Key Business Highlights

FDA BLA Approval — A Transformative Milestone

In December 2025, the FDA approved the Biologics License Application (BLA) for Avance, making it the first and only FDA-approved biologic for treating peripheral nerve discontinuities with 12 years of U.S. market exclusivity . CEO Dale called it "the most significant milestone in AxoGen's history" .

Management is leveraging this milestone across four fronts :

- Customer engagement — reinforcing confidence in Avance's safety and efficacy

- Payer engagement — driving toward near-universal U.S. coverage

- Clinical advancement — enabling prioritized studies under approved framework

- Manufacturing investments — supporting scalability under one quality system

Reimbursement Tailwinds

- CMS created a new Level 3 Nerve Procedure Code effective January 1, 2026

- Hospital outpatient reimbursement increased 40% YoY

- Added ~19.8 million newly covered lives in 2025

- Commercial payer coverage now exceeds 65%

- Management expects BLA will help address remaining payer objections; targeting universal coverage by 2028

Balance Sheet Strengthened

- Raised $133.3 million via public offering (January 2026)

- Fully repaid $69.7 million Oberland term loan

- Cash, restricted cash, and investments: $45.5 million at year-end

Commercial Expansion

Management outlined aggressive growth plans across all segments :

2026 HiPo Account Targets :

- 60% of revenue growth from high-potential accounts

- 18% productivity growth in HiPo accounts

- Activate at least 100 new surgeons

2026 Training Objectives :

- Extremities: 10 programs, 200 surgeons trained

- OMF/Head & Neck: 6 programs, 100 surgeons trained

- Breast: 5 programs, 75 surgeon pairs trained

Full Year 2025 Summary

Despite the Q4 noise, full-year 2025 showed strong operating leverage with Adjusted EBITDA margins expanding to 12.4% from 10.6% .

Segment Performance

Revenue growth was broad-based with double-digit gains across all markets :

High-potential (HiPo) accounts drove 61% of growth, with average HiPo account productivity up 21% .

Forward Catalysts

- 2H 2026: Meaningful prostate clinical signals expected

- 2H 2028: Management targeting near-universal U.S. payer coverage

- 2026: R&D updates on therapeutic reconstruction program

- Ongoing: BLA enables prioritized breast & mixed/motor nerve studies

Q&A Highlights

On Guidance Conservatism

When asked about the "at least 18%" revenue growth guidance versus 21% exit rate, CEO Michael Dale characterized it as "prudent" rather than conservative: "We're building off of a larger base. We believe that our commercial customer creation models are elastic, but they still need to be managed. Each quarter is a new quarter, each year is a new year."

On Gross Margin Cadence

CFO Lindsay Hartley provided important color on margin timing: Gross margin pressure will build through 2026 as the company transitions to selling Avance as a biologic product starting Q2. "As we progress through the year and we begin selling the new biologic Avance product, it will carry a heavier cost... we expect to see that pressure in Q2 and going into the remaining second half of the year." Improvement expected to begin in 2027 .

On Clinical Trial Strategy

Management outlined differentiated approaches by indication :

- Mixed/motor nerves: Randomized clinical trials required

- Breast: Unlikely randomized (considered "unethical" given current evidence); focused on patient fit and response rates

- Prostate: Study design to be determined after clinical signals emerge from 100+ initial procedures

On Revenue Per Patient

CEO Dale provided helpful ASP hierarchy across indications :

- Breast: Highest ASP due to longer grafts (1-2mm diameter, 7mm length) and multiple grafts used

- Prostate: Relatively higher ASP (4-5mm diameter, ~50mm length grafts)

- Extremities: Lower ASP on average, though trauma cases can match breast

On Market Penetration

Despite 130 extremities reps planned, Dale emphasized this represents only partial coverage: "If you wanted to provide full coverage for extremities, you'd probably need somewhere between 400-600 sales representatives... We're a long way from full coverage." Breast organization could "as much as double between now and 2028 and 2029" .

On BLA Transition Impact

The tissue-to-biologic transition will be "invisible to the customer" with no inventory obsolescence risk .

Bottom Line

Axogen delivered on revenue growth (+21% YoY) but disappointed on profitability due to one-time FDA BLA approval costs. The 11% after-hours drop appears to reflect both the EBITDA miss and sequential revenue decline after Q3's record quarter. However, the fundamental thesis remains intact: FDA BLA approval provides 12 years of exclusivity, reimbursement is improving, and 2026 guidance of at least 18% growth exceeds Street expectations. The key question is whether the stock's 280%+ run from its lows has already priced in most of the good news.

Data sourced from Axogen 8-K and Q4 2025 earnings call transcript filed February 24, 2026, and S&P Global.